Commercial Pulse Report | 1-14-2025

Experian has just released the Commercial Pulse Report for January 14th, 2025 which includes a compelling look at the leisure and hospitality sector.

The Leisure & Hospitality sector has long been one of the hardest-hit industries following the COVID-19 pandemic. But in 2024, it demonstrated impressive resilience and recovery, with data from the latest report highlights several noteworthy trends that mark a turning point for this vital sector of the economy.

Watch Our Commercial Pulse Update

Travel Reaches New Heights

Air travel soared to record-breaking levels in 2024, with the TSA screening over 903 million passengers—a 6.5% increase from pre-pandemic levels. This rise reflects not just pent-up travel demand but also growing consumer confidence in the safety and accessibility of travel.

Hotel occupancy rates, while recovering, still lag slightly behind pre-pandemic levels. Reduced corporate travel and the rise in remote work have contributed to this trend. However, leisure travel remains strong, and small businesses in the travel ecosystem are seeing the benefits.

Stabilizing Credit Activity and Improved Risk Scores

On the commercial credit side, there’s good news. Businesses in the Leisure & Hospitality subsectors have experienced a gradual increase in new account inquiries, and credit risk scores have steadily improved since late 2023. These metrics indicate a promising stabilization of credit activity.

Interestingly, the average number of commercial credit accounts per business continues to decrease. This could reflect cautious financial planning as businesses strive to balance growth with sustainable debt.

Consumer Trends Drive Growth

The affordability of travel is another major driver of the sector’s recovery. Inflation in the travel sector has trended lower than the broader economy, making vacations and leisure activities more accessible for many consumers. Despite financial pressures, such as a significant portion of Americans living paycheck-to-paycheck, this trend has supported a surge in travel demand.

Challenges Remain

While the outlook is positive, challenges persist. For example, delinquency rates within the sector fluctuate month to month, although no long-term trend of increased risk has been observed. The Hotel, RV, and Campground subsector, which bore the brunt of the pandemic’s impact, now boasts the lowest charge-off rate among Leisure & Hospitality categories—a testament to its steady recovery.

There’s a lot more on the leisure and hospitality study in this week’s report, so download your copy today!

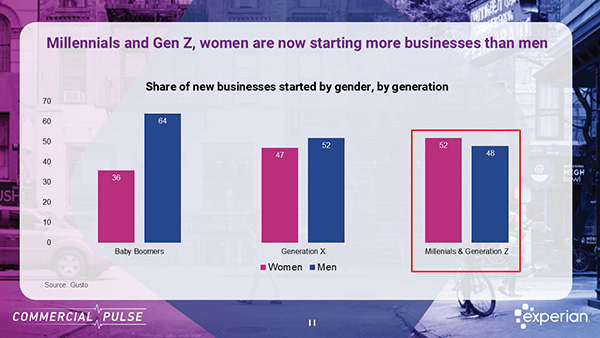

Women-Owned Small Businesses: Growth, Credit Behavior, and Risk Implications for Lenders A fast-growing segment, women-owned businesses bring unique credit dynamics shaped by size, lifecycle, and access to capital. Understanding these differences is key to improving risk accuracy and capturing growth. This week, the Commercial Pulse Report takes a closer look at Women-owned small businesses, and there's a lot to be excited about. Watch The Commercial Pulse Update Women-owned businesses are no longer a niche segment—they are a defining force in the evolution of the U.S. small business landscape. Today, they account for nearly half of all new business formations and generate approximately $2.7 trillion in annual revenue. For Chief Risk Officers and credit risk teams, this growth presents both opportunity and complexity. The structural and behavioral differences of women-owned businesses introduce new considerations for underwriting, portfolio management, and long-term risk strategy. A Rapidly Expanding—but Structurally Distinct—Segment The growth trajectory of women-owned businesses is undeniable. In 2025 alone, women owned more than 14 million businesses in the U.S.—nearly double the total from two decades ago. However, this expansion is not simply a scaled version of traditional small business growth. Women-owned firms tend to be: More concentrated in service-oriented industries Smaller in size, with lower average revenue Earlier in their business lifecycle These characteristics matter from a risk perspective. Younger businesses inherently carry higher uncertainty, shorter credit histories, and less established operating resilience. For underwriting teams, this means traditional risk models—often calibrated on more mature firms—may underrepresent or misclassify risk in this segment. Credit Access and Capital Structure: A Different Funding Model One of the most important distinctions lies in how women-owned businesses access capital. Compared to male-owned businesses, women entrepreneurs: Seek less commercial credit overall Rely more heavily on personal networks such as friends and family Utilize credit cards and online lenders more frequently than traditional bank financing They also tend to have fewer commercial trade lines and lower credit limits. At first glance, this could be interpreted as weaker credit demand. In reality, it often reflects structural barriers to access, differences in borrowing preferences, and earlier-stage business profiles. For CROs, this raises a critical question:Are current underwriting frameworks capturing true risk—or simply reflecting historical access inequalities? Utilization and Discipline: A More Nuanced Risk Signal Despite lower credit limits and fewer trade lines, women-owned businesses exhibit similar credit utilization rates compared to male-owned businesses. This is a crucial insight. Equivalent utilization, despite constrained access to credit, suggests: Strong credit discipline Efficient use of available capital Potential unmet demand for additional financing From a risk modeling perspective, utilization alone may not be a sufficient differentiator. Instead, it should be evaluated alongside capacity constraints and growth intent. This creates an opportunity for lenders to refine segmentation strategies—identifying businesses that are not overextended, but rather underserved. Delinquency and Credit Performance: Stability with Key Gaps From a performance standpoint, the data offers a more balanced view. Delinquency rates between women- and male-owned businesses are comparable, indicating similar repayment behavior across segments. However, average commercial credit scores for women-owned businesses remain slightly lower. This gap is largely driven by: Shorter credit histories Fewer active trade lines Lower overall credit exposure Encouragingly, the credit score gap has begun to narrow in recent months. For risk leaders, this suggests that observed differences in credit scoring are less about elevated risk and more about data depth and credit maturity. This distinction is critical when designing underwriting policies that balance inclusion with risk controls. Generational Momentum and Future Portfolio Impact Another dynamic shaping this segment is generational. Among Millennials and Gen Z, women are now starting more businesses than men. This shift is driven by motivations such as: Flexibility and autonomy Desire for control over work schedules Pursuit of entrepreneurial independence For lenders, this signals that the influence of women-owned businesses will not only persist—but accelerate. As these younger businesses mature, they will transition into larger credit exposures, more complex financing needs, and deeper integration into commercial credit ecosystems. The decisions made today around underwriting, access, and segmentation will directly shape the future risk profile of portfolios. Implications for Risk Strategy and Underwriting For Chief Risk Officers and their teams, the rise of women-owned businesses presents a clear mandate: evolve risk frameworks to reflect a changing borrower base. Key considerations include: Reassessing underwriting models to account for thinner credit files and shorter business histories Incorporating alternative data to better evaluate early-stage businesses Differentiating between constrained access and true risk exposure Monitoring portfolio diversification as this segment grows in share Importantly, this is not simply a question of expanding access. It is about improving risk accuracy. Misinterpreting structural differences as elevated risk can lead to missed growth opportunities, while failing to account for lifecycle dynamics can introduce unintended exposure. Balancing Growth and Risk in a Changing Landscape Women-owned businesses represent a fast-growing, resilient, and evolving segment of the economy. They are reshaping patterns of credit demand, challenging traditional assumptions, and creating new opportunities for lenders. At the same time, they require a more nuanced approach to risk assessment—one that recognizes the interplay between business maturity, access to capital, and credit behavior. For CROs, the path forward is clear: leverage data, refine models, and align risk strategy with the realities of today’s small business landscape. Learn more ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis. ✔ Subscribe to our YouTube channel for regular updates on small business trends. ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow. Download the Commercial Pulse Report Visit Commercial Insights Hub Related Posts

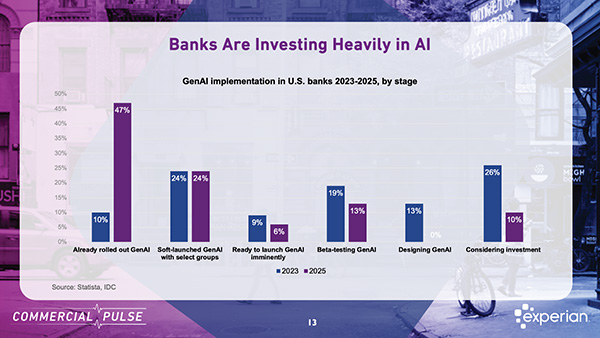

How Structural Shifts in Scale, Technology, and Customer Behavior Are Redefining Risk Leadership This week’s Experian Commercial Pulse report includes great insights on the banking industry, a sector that is not simply evolving, it's structurally transforming. The implications of banking transformation extend well beyond portfolio performance. Consolidation, digital acceleration, and aggressive investment in artificial intelligence are reshaping the competitive landscape and redefining risk management itself. Watch The Commercial Pulse Update While commercial credit performance remains relatively stable, the operating model of banking is changing quickly. The institutions that thrive in this environment will be those that modernize risk frameworks in parallel with ongoing structural change. This week's Pulse identified four major trends CRO's and risk teams should be watching closely. 1. Consolidation in the Banking Industry: Fewer Banks, Fewer Branches The number of FDIC-insured banks has declined to less than half of what it was in 2000. Decades of mergers and acquisitions, including several of the largest transactions occurring in just the past five years, have materially reshaped the competitive environment. At the same time, the physical footprint of banking has contracted. Total branch counts have fallen significantly from their 2008 peak, and branch availability continues to decline across many regions. For risk leaders, consolidation creates both opportunity and exposure. On one hand, scale can improve capital efficiency, risk diversification, and investment capacity in advanced analytics. Larger institutions may also benefit from deeper data pools and stronger enterprise risk infrastructures. On the other hand, concentration risk becomes more pronounced, geographically, sectorally, and operationally. As institutions grow through acquisition, integration risk, model harmonization challenges, and cultural alignment issues must be carefully managed. For CROs, consolidation is not just an industry headline, it is a structural variable influencing counterparty exposure, competitive pressure, and systemic interdependencies. 2. The Acceleration of Online Banking As physical branches decline, digital engagement has accelerated dramatically. In 2019, just over half of U.S. consumers used online banking. By 2025, that number rose to roughly 71%, and projections suggest it could approach 80% by 2029. Younger demographics in particular show a strong preference for online-only banking relationships, while older customers continue to rely more heavily on traditional channels. For small businesses, digital onboarding, online treasury management, mobile payments, and remote lending processes are no longer differentiators — they are expectations. For CROs, increased digital penetration changes the risk equation in several ways: Fraud vectors expand as digital interactions multiply. Identity verification and authentication controls become mission-critical. Real-time monitoring replaces periodic review. Data velocity increases, requiring scalable analytics infrastructure. Operational resilience also becomes more important. As customer engagement concentrates in digital channels, system uptime, cybersecurity, and third-party risk management move to the forefront of enterprise risk oversight. Digital adoption is not merely a distribution channel shift. It is a transformation in how risk manifests and must be measured. 3. Technology Trends: AI, Automation, and Real-Time Risk Intelligence Technology modernization has become central to competitive strategy across commercial banking. Artificial intelligence, machine learning, real-time fraud detection, and automated underwriting are moving from pilot programs into core production environments. Generative AI adoption in particular has accelerated rapidly, with nearly half of commercial banks now operating some form of GenAI solution in production. For a CRO, the opportunity is substantial. Advanced analytics can: Enhance early warning systems for credit deterioration. Improve fraud detection accuracy while reducing false positives. Refine borrower segmentation and pricing precision. Optimize collections prioritization and recovery strategies. Strengthen stress testing and scenario modeling capabilities. However, innovation introduces new forms of model risk. AI-driven decisioning must be explainable, auditable, and compliant with regulatory expectations. Governance frameworks must evolve to ensure transparency, fairness, and mitigating bias. Data lineage and model validation processes must remain rigorous even as deployment speeds increase. The challenge for risk leaders is achieving balance, leveraging technological advantage without compromising control discipline. 4. Investment in AI: Strategic Imperative, Not Experimentation AI investment in commercial banking is accelerating at a notable pace. Industry forecasts indicate that AI spending in the Americas banking sector could exceed $54 billion by 2028 — nearly tripling from 2024 levels. This level of capital allocation signals a fundamental shift: AI is no longer viewed as an incremental enhancement. It is considered foundational infrastructure. Executives report that AI initiatives are focused on: Cybersecurity enhancement Fraud detection and prevention Operational efficiency Customer engagement personalization Credit risk modeling improvement For CROs, this scale of investment demands disciplined oversight. Key considerations include: Are AI initiatives aligned with defined risk appetite statements? Is governance keeping pace with deployment velocity? Are internal teams sufficiently trained to interpret AI outputs? Is the institution prepared for heightened regulatory scrutiny around automated decisioning? The strategic sweet spot lies in controlled acceleration — modernizing the risk stack while reinforcing control frameworks. Final Perspective for CROs Commercial credit performance today remains relatively stable. Yet the true story in banking is not short-term performance, it is long-term transformation. We are operating in an environment defined by structural consolidation, digital-first customer behavior, rapid AI adoption, expanding data ecosystems, and increasing regulatory complexity. For Chief Risk Officers, the mandate is clear: safeguard portfolio quality while modernizing risk infrastructure. The institutions best positioned for sustainable growth will not simply extend capital efficiently, they will integrate advanced analytics, strengthen governance, and proactively manage emerging digital risks. Transformation is underway. The question is not whether it will continue. The question is whether risk organizations will lead it — or react to it. Learn more ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis. ✔ Subscribe to our YouTube channel for regular updates on small business trends. ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow. Download the Commercial Pulse Report Visit Commercial Insights Hub Related Posts

Experian's Construction Industry Risk Model Offers Greater Precision for CRO's Construction is building momentum in 2026 — but capital is becoming more selective just as demand accelerates. For Chief Risk Officers, this is not simply a growth story. It is a risk calibration moment. For Chief Risk Officers and commercial lenders, that combination creates a complex credit environment: expanding opportunity on one hand, rising sector-specific risk on the other. This week’s Commercial Pulse Report highlights why construction deserves close attention — and why traditional risk tools may not be sufficient in the current cycle. Watch The Commercial Pulse Update A Growing Sector with Structural Tailwinds Construction contributes approximately 4.8% of U.S. GDP and remains a foundational industry supporting infrastructure modernization, AI-powered data centers, renewable energy expansion, and multifamily housing demand. Since Q1 2013, the number of construction firms in the U.S. has grown by 28%, reaching nearly 950,000 establishments. Employment in the sector has increased 49% since January 2010, reflecting both demand expansion and increased new business formation. Construction spend peaked at just over $2.2 trillion in April 2024, contracted 3.3% in 2025, and is forecast to rebound 7% in 2026 to exceed $2.1 trillion. Construction businesses seek credit more than twice as often as companies in many other industries — a structural dynamic that fundamentally alters how risk signals should be interpreted. From a growth perspective, the fundamentals remain solid. Non-residential construction is particularly strong, driven by: AI-powered data center buildouts Renewable energy infrastructure Public infrastructure modernization Regional population and job growth For lenders, that growth trajectory signals continued credit demand — especially for working capital, equipment financing, and project-based lending. But growth alone doesn’t define risk. Payment Friction Is Structurally Embedded While construction is expanding, it is also experiencing persistent cash flow strain. According to a 2025 industry study referenced in the report: 70% of contractors regularly face delayed payments 41% have increased their use of credit to manage cash flow 1 in 4 contractors have reduced bidding activity due to financial strain Top contributors to payment delays include: Cash flow constraints Contract disputes Administrative inefficiencies Banking and financing delays Technology and process friction Construction projects are capital-intensive and milestone-driven — meaning liquidity depends on payment timing, not just performance. When developers delay payments, the effects cascade through subcontractors and suppliers. For lenders, this creates a recurring risk pattern: strong backlog with fragile cash flow. For CROs, this creates a distinct risk profile: businesses may show strong top-line growth but experience liquidity stress due to payment timing — increasing reliance on revolving credit and short-term financing. Construction Businesses Seek and Use More Credit Experian data reveals that construction businesses: Seek commercial credit more than twice as often as non-construction businesses Maintain a higher average number of commercial trades Exhibit higher 60+ day delinquency rates compared to other industries At the same time, commercial lenders continue reporting tightened underwriting standards, particularly for small firms. This dynamic — structurally elevated credit demand colliding with tighter credit conditions — increases the need for precise risk interpretation. Elevated inquiries and higher trade counts in construction are not inherently distress signals. In many cases, they reflect the capital-intensive, project-based nature of the industry. The risk is not high credit usage — the risk is misinterpreting what that usage signals. Construction firms are not homogenous. Risk varies significantly across: Trade specialty Project mix (residential vs. non-residential) Business maturity Regional economic exposure Capital structure and utilization patterns Generic commercial risk scores may not fully capture these industry-specific nuances, increasing the potential for both over- and under-estimating risk within construction portfolios. Why Generic Risk Models Fall Short in Construction Construction presents several characteristics that can distort traditional risk assessments: High inquiry and trade activity – Elevated credit usage may reflect normal operating structure, not necessarily distress. Cyclical delinquency patterns – Project-based payment timing can temporarily inflate delinquency metrics. Industry-specific trade relationships – Supplier networks and payment practices differ from other sectors. Material cost volatility – Construction input costs have tripled since the early 1980s and remain elevated relative to pre-pandemic levels. When underwriting models are calibrated to all industries collectively, they may under- or over-estimate risk within construction portfolios. In tightening credit cycles, imprecision compounds faster: Constraining high-quality borrowers Underpricing volatile segments Misallocating capital For CROs, this is not theoretical — it is a margin issue. The Case for Industry-Specific Risk Modeling Addressing this requires industry-calibrated analytics — models built specifically to reflect construction trade behavior and payment dynamics. For example, Experian developed the Small Business Credit ShareTM model for Construction — a purpose-built commercial risk score tailored specifically to businesses with construction trades. The model: Uses advanced machine learning methodology (XGBoost) Predicts the likelihood of becoming 61+ days beyond terms within 12 months Incorporates aggregate business data, public records, trade data, and construction-specific attributes Produces a score range of 300 to 850, where higher scores indicate lower risk Performance testing shows improved KS and GINI separation compared to generic all-industry models, as well as stronger bad capture rates in the lowest scoring deciles. In practical terms, that means: Better identification of high-risk borrowers Improved differentiation among mid-tier applicants More confident credit line sizing Smarter portfolio monitoring For lenders balancing growth objectives with capital discipline, industry-optimized analytics can materially improve decision accuracy. Learn More about Experian SBCS Construction Score Strategic Implications for Chief Risk Officers As we move further into 2026, construction presents a paradox: – Strong sector growth – Elevated credit demand – Tightening lending standards – Persistent payment delays – Increased reliance on alternative capital The strategic question for CROs is not whether to participate in construction lending — it is how to do so with precision. Key considerations include: Are your underwriting models calibrated to sector-specific risk patterns? Are you distinguishing between structural credit usage and distress signals? Are portfolio limits aligned to trade-level risk differentiation? Are you leveraging machine learning where appropriate to isolate “bads” earlier? In a tighter credit market, competitive advantage often comes from accuracy — not volume. Growth Requires Discipline Construction will remain a critical growth engine for the U.S. economy in 2026. Demand is real. Infrastructure investment is accelerating. Capital needs are expanding. But so are constraints. For lenders and risk leaders, the opportunity lies in balancing participation with discipline — using analytics sophisticated enough to separate resilient operators from liquidity-stressed borrowers. The cranes are rising.Capital is tightening. In 2026, growth will be available. Precision will be decisive. Learn more ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis. ✔ Subscribe to our YouTube channel for regular updates on small business trends. ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow. Download the Commercial Pulse Report Visit Commercial Insights Hub